Earlier this year, Boston Consulting Group (BCG) released a groundbreaking report commissioned by Third Way and Breakthrough Energy finding that strategic investments in six key clean energy technologies could yield massive and lasting benefits for the US economy.

Why the US Should Compete in the EV Market

Earlier this year, Boston Consulting Group (BCG) released a groundbreaking report commissioned by Third Way and Breakthrough Energy finding that strategic investments in six key clean energy technologies could yield massive and lasting benefits for the US economy. Of the six technologies BCG analyzed, electric vehicles (EVs) represented the biggest economic opportunity by far.

And for good reason: The global transition to EVs is well underway, with EV sales worldwide doubling between 2020 and 2021. The transition comes with tremendous opportunity for US automakers and suppliers to capture tens of trillions of dollars in market value and create hundreds of thousands of jobs between now and 2050—by far the largest market potential of any technology BCG analyzed—while providing consumers with cleaner, more affordable cars.

But it also comes with risk: China’s dominance over critical mineral extraction and processing and battery production has left US companies susceptible to supply chain disruptions and threatens their standing as leaders in this industry.

At the same time, the dawn of autonomous and connected vehicle technologies is closely tied to the EV transition as customers expect increasingly connected features in their vehicles. This creates additional opportunity for US software developers and aftersales service providers—two areas where the US can maintain and grow its existing competitive advantage.

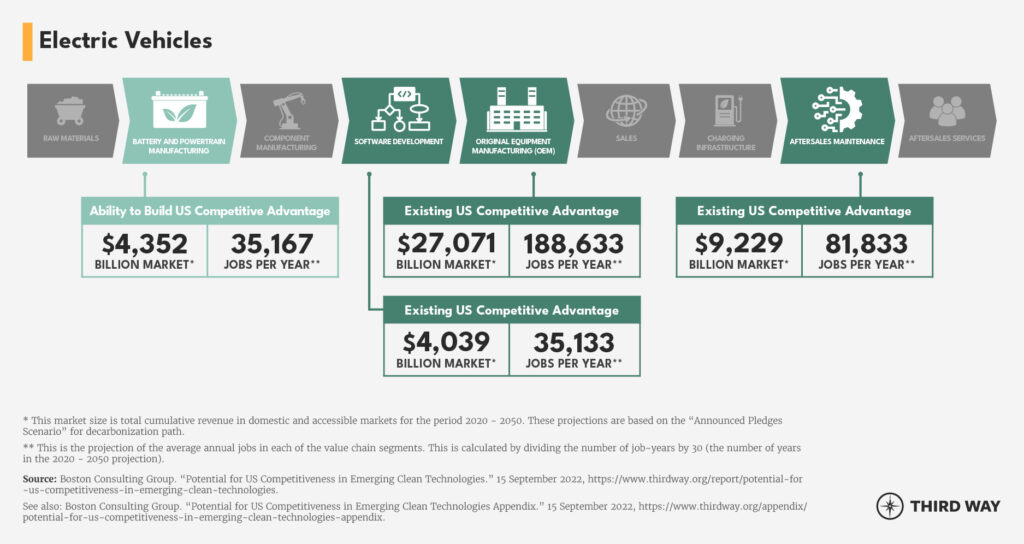

BCG’s analysis of the EV value chain identified the four most compelling segments based on market size and the potential for US competitiveness: battery and powertrain manufacturing, original equipment manufacturing (OEM), software development and aftersales services. The US already holds a competitive advantage in some of these segments and with the right policies can grow that advantage. BCG found a large serviceable addressable market (SAM)—the total global market excluding countries where US exports are unlikely due to political or economic barriers1—across these key segments, amounting to as much as $1.06 trillion annually by 2050 thanks to the massive global demand for automobiles and significant public and private investment in vehicle electrification.

BCG also found significant job potential in these four value chain segments, with the US able to compete for as many as 10.2 million jobs between 2020 and 2050. This will include a range of different jobs, from jobs in battery production and EV assembly plants that don’t require higher levels of education, to high-income jobs in software development that require college degrees.

In addition to these four key value chain segments, we also include raw materials in this report. While BCG did not identify raw materials as a value chain segment where the US could have a competitive advantage, we opted to include it given its importance to the entire supply chain and the risks associated with China’s dominance over this segment.

Read the full article by Third Way here.